|

2011-6-24

The Change

But over the next two weeks, there was a sharp drop in New York futures, with July falling a total of 1,828 points by June 16 to close at 145.96 cents, and December falling a total of 1,905 points to close at 120.18 cents. There are a few reasons outside the cotton trade that are influencing this development: for example, the uncertainty with the euro, including the Greek debt crisis. Probably other countries will follow, as has been mentioned in all important financial newspapers.

However, according to Plexus, "demand in the physical [cotton] market has basically been non-existent lately. Mills are still trying to digest high-priced inventories of cotton, yarn and fabrics and with the huge price swings we have seen in recent months, there is a lot of confusion as to where a sustainable price level for cotton really is.

"The latest US export sales report was actually a pleasant surprise after 11 consecutive weeks of negative numbers in current crop. Net sales of Upland and Pima cotton amounted to 10,300 running bales for this season and 39,200 running bales for next marketing year. Shipments of 227,100 running bales reduced the outstanding balance for the current marketing year to just 2.2 million running bales (last year 3.4 million bales) and ... at the current pace of shipment all the inventory would be gone by September."

Rebound Of Global Stocks Reported

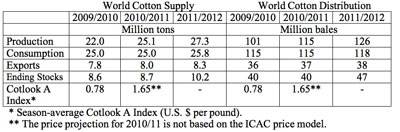

Also, on June 1, ICAC was reporting a rebound of global cotton stocks in 2011/12, noting that "This season started with a firm demand from spinning mills, which were looking to rebuild their stocks depleted in 2009/10, but is ending with weaker demand, mainly due to high cotton prices." The following table showing world cotton supply and distribution, provided by ICAC, is self-explanatory:

ICAC reported: "Global mill use is expected to resume increasing in 2011/12, driven by a projected robust global economic growth and boosted by increased production, but moderated by relatively high cotton prices and competition from chemical fibers. ... The world ending stocks-to-use ratio could rebound to 40% in 2011/12. "The Secretariat believes that the season-average Cotlook A Index will decline significantly in 2011/12, although it will probably remain above the ten-year average of $0.60 per pound." Tight Supplies However, as Plexus noted on June 16, "remaining supplies in the US are very tight and may not be enough to meet existing export commitments until October, plus the coming US crop is in trouble and may yield several million bales less than what was expected just a month or two ago ...." And what exactly is the annual demand: 119 million or 114 million bales? Again, the heat is on. Source:Textile World

|

浙公網(wǎng)安33010602010414

浙公網(wǎng)安33010602010414